The transformer is heavy in material and light in work, and the cost ratio of raw materials is significant

The upstream industry of power transformer manufacturing industry is silicon steel sheet, copper, aluminum and other non-ferrous metals and other raw materials. Transformer raw materials constitute the main cost of the industry. For general power transformer, silicon steel accounts for 35% of the total cost of raw materials, copper accounts for 30%, insulation materials accounts for 15%, plate accounts for 10%, and other materials account for 10%. Transformer is an industry with heavy material and light industry. The material cost accounts for more than 60% of the final cost price of the whole product.

Chart 1: raw material cost structure of power transformer (unit:%)

</strong>")

Source: collected by prospective industry research institute

The growth of electricity consumption and installed capacity drives the development of the industry

Residential electricity also has a great impact on the power transformer industry. China has a large population, rapid urbanization process, continuous improvement of living standards, and increasing demand for electricity, which puts forward higher requirements for power grid construction and promotes the development of power transformer manufacturing industry.

In 2017, the electricity consumption of the whole society was 6307.7 billion kwh, with a year-on-year increase of 6.6%. In terms of industries, the power consumption of the primary industry was 115.5 billion kwh, an increase of 7.3% year-on-year; that of the secondary industry was 4441.3 billion kwh, an increase of 5.5%; that of the tertiary industry was 881.4 billion kwh, an increase of 10.7%; and that of urban and rural residents was 869.5 billion kwh, an increase of 7.8%.

Figure 2: electricity consumption and growth of China from 2010 to 2017 (unit: trillion kwh,%)

</strong>")

资料来源:前瞻产业研究院整理

电力变压器制造行业的下游用户主要包括电力系统及其他需要自行建设电力网络的行业(如石油、化工、矿山、冶金、铁路等)的供电部门,其中电力行业的发展状况将对本行业产生重大影响。

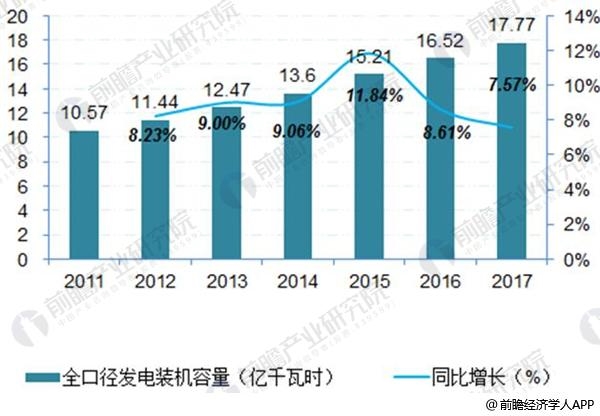

2017年末全国发电装机容量177703万千瓦,比上年末增长7.57%。其中火电装机容量110604万千瓦,增长4.3%;水电装机容量 34119万千瓦,增长2.7%;核电装机容量3582万千瓦,增长6.5%;并网风电装机容量16367万千瓦,增长10.5%;并网太阳能发电装机容量13025万千瓦,增长68.7%。电源结构继续优化,绿色比例上升。

图表3:2011-2017年全国全口径发电设备容量(单位:亿千瓦时,%)

Source: collected by prospective industry research institute

Power transformer industry is a typical investment promotion industry. Considering only the domestic market, domestic power investment determines the rise and fall of the power transformer industry, in which power plants and power grid constitute two major types of customers. In particular, power grid companies have a huge demand from the most high-end 1000kV UHV Transformer to the lowest 10kV distribution transformer.

From 2011 to 2017, the overall sales revenue of power transformer industry showed an upward trend. In 2016, the sales revenue of power transformer industry reached 272.675 billion yuan, a year-on-year increase of 12.24%. In 2017, the sales revenue of power transformer industry reached 269.355 billion yuan, a year-on-year decrease of 1.22%.

Table 4: trend chart of sales revenue and growth rate of power transformer industry from 2011 to 2017 (unit: 100 million yuan,%)

</strong>")

Source: collected by prospective industry research institute

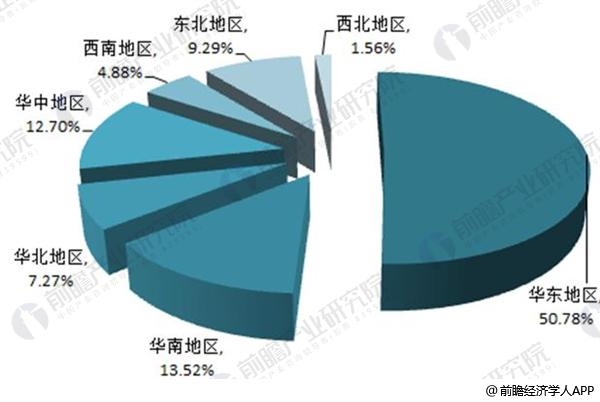

There is regional imbalance in the development of the industry

There are obvious regional differences in the development of power transformer manufacturing enterprises in China. The production bases of main enterprises are concentrated in East China and South China. Among them, East China accounts for 50.78% of the total number of power transformer manufacturing enterprises in China, and South China and central China account for 13.52% and 12.7% of the total number of power transformer manufacturing enterprises in China. However, the number of enterprises in Northeast, north, southwest and northwest regions accounted for less than 10%.

Figure 5: regional distribution of power transformer manufacturing enterprises in China in 2017 (unit:%)

Source: collected by prospective industry research institute

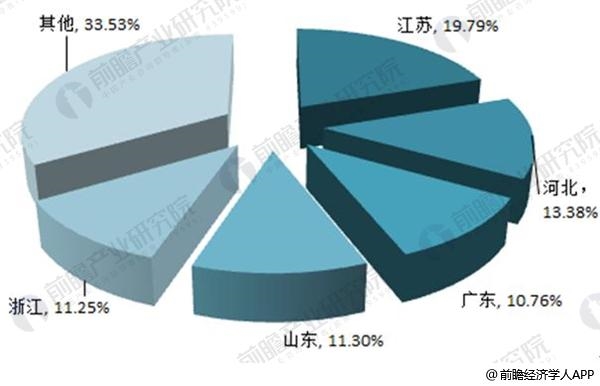

The production capacity of China's power transformer manufacturing industry is also extremely unbalanced in all major regions of the country. The proportion of finished products in Jiangsu Province is as high as 19.79%, indicating that the regional concentration of China's power transformer manufacturing industry is high. Second, Hebei and Shandong accounted for 13.38% and 11.30% respectively, and Zhejiang also accounted for 11.25%. The top five regions accounted for 66.48%.

Figure 6: regional composition of finished products in China's power transformer manufacturing industry in 2017 (unit:%)

Source: collected by prospective industry research institute

The above data and analysis are from the report on market demand forecast and investment strategic planning of China's power transformer industry from 2018 to 2023 issued by prospective industry research institute.

Service

Service